If you want the short version, here it is: the latest official data shows that Falkland Islands tourism has recovered strongly, cruise continues to dominate total visitor volume, and land-based leisure travel now carries more economic weight per visitor than raw arrival numbers suggest.

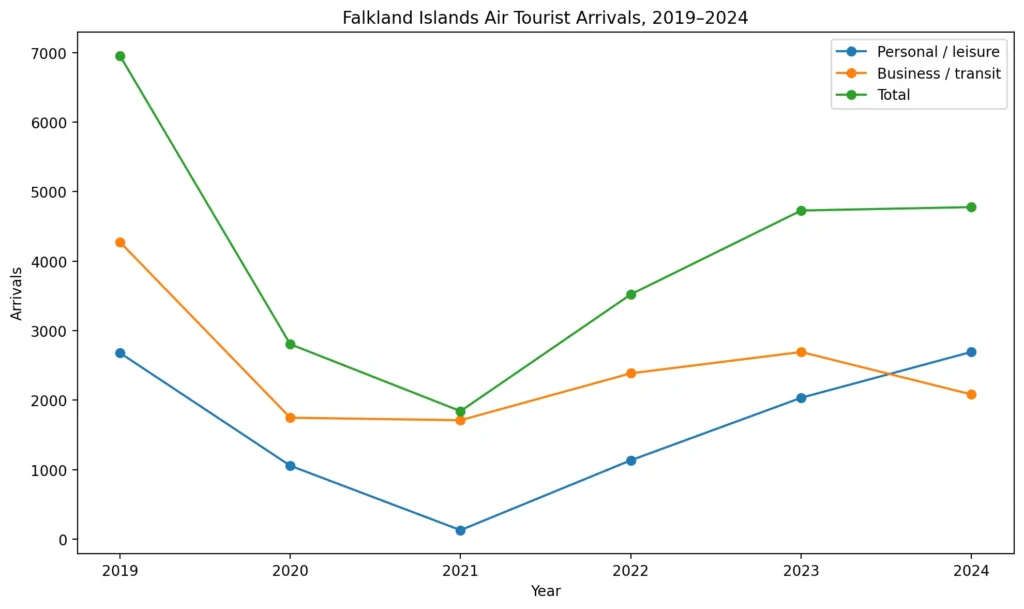

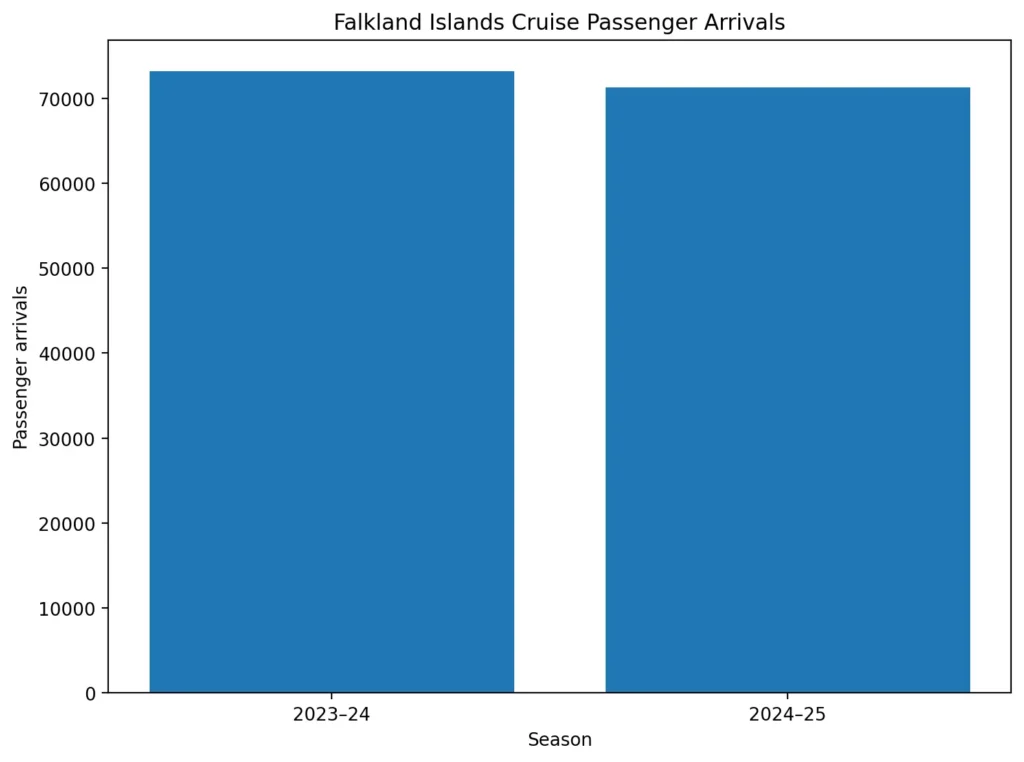

The newest annual figures show 2,695 land-based leisure visitors in 2024, 4,778 total air tourists for all purposes, and 71,278 cruise passenger arrivals in the 2024–25 season. Combined direct expenditure from land-based visitors, domestic visitors, and cruise visitors came to more than £16.1 million. According to the official Falkland Islands Statistics Report 2024, the recovery from the pandemic now looks complete, even though spending patterns softened in some parts of the market.

This page is built as a reference asset. It pulls together the most useful numbers from the official annual tourism reports, adds context where the figures matter, and flags one or two areas where the public data needs to be read carefully. The main sources are the official Falkland Islands Statistics Report 2024, the previous Falkland Islands Statistics Report 2023, and the Falkland Islands Tourist Board’s statistics archive.

Key Falkland Islands travel statistics at a glance

Here are the numbers most people want first.

| Metric | Latest official figure |

|---|---|

| Total land-based tourists, all purposes, 2024 | 4,778 |

| Land-based leisure visitors, 2024 | 2,695 |

| Average leisure length of stay, 2024 | 14.5 nights |

| Leisure visitor spend, 2024 | £6.9 million |

| Cruise passenger arrivals, 2024–25 | 71,278 |

| Average cruise spend per passenger, 2024–25 | £79.80 |

| Total cruise passenger spend, 2024–25 | £5.5 million |

| Domestic tourism trips, 2024 | 10,896 |

| Combined direct expenditure | Over £16.1 million |

All of those figures come from the official Falkland Islands Statistics Report 2024.

What the latest annual data says

The biggest headline is not just recovery. It is recovery with a different balance of value and volume.

The official 2024 report says 2024 was the second-highest year on record for land-based leisure visitors after 2007, with 2,695 leisure arrivals. At the same time, cruise traffic remained extremely large, though the 2024–25 season was slightly lower than the record 2023–24 season.

The Falklands are now seeing strong demand on both sides of the market, but the shape of that demand is not identical. Cruise brings the crowd. Land-based travel brings the deeper stay.

The report also shows that total land-based tourist arrivals for all purposes rose to 4,778 in 2024, up just 1.0% on 2023. That smaller overall increase happened because business and transit arrivals dropped, even while personal or leisure arrivals jumped sharply.

In fact, the report notes that business arrivals fell 22.7% and still accounted for 43.6% of all tourist arrivals in 2024 under the UNWTO definition used in the report. That is a useful reminder that the air-arrival market is not a clean leisure-only dataset.

Land-based tourism recovered strongly in 2024

For pure visitor experience and trip-planning value, land-based leisure is the most important section of the dataset.

According to the official 2024 report, leisure arrivals rose from 2,035 in 2023 to 2,695 in 2024, which is a 32.4% increase. That put land-based leisure slightly above pre-COVID 2019, when the islands recorded 2,681 personal arrivals. If you zoom out further, the long-term chart in the same report shows 2024 as one of the strongest air-leisure years in the last quarter century.

That matters because air visitors do not just pass through. The same report puts the average leisure stay at 14.5 nights, up more than two days on the previous year. So even without forcing complicated economics into the picture, the data already tells a simple story: fewer people than cruise, but much longer presence on the ground.

The previous 2023 report is useful here because it shows how sharp that rebound really was. It recorded 1,806 leisure visitors in 2023, already a strong recovery year. The move from 1,806 to 2,695 in one year is not just noise. It is a substantial step up.

Cruise tourism still drives the biggest visitor volume

If land-based travel defines trip depth, cruise defines total reach.

The official 2024 report says the 2024–25 cruise season recorded 71,278 passenger arrivals, down from the record 73,191 in 2023–24. Even with that slight decline, the report still calls 2024–25 the third best cruise season on record by arrivals.

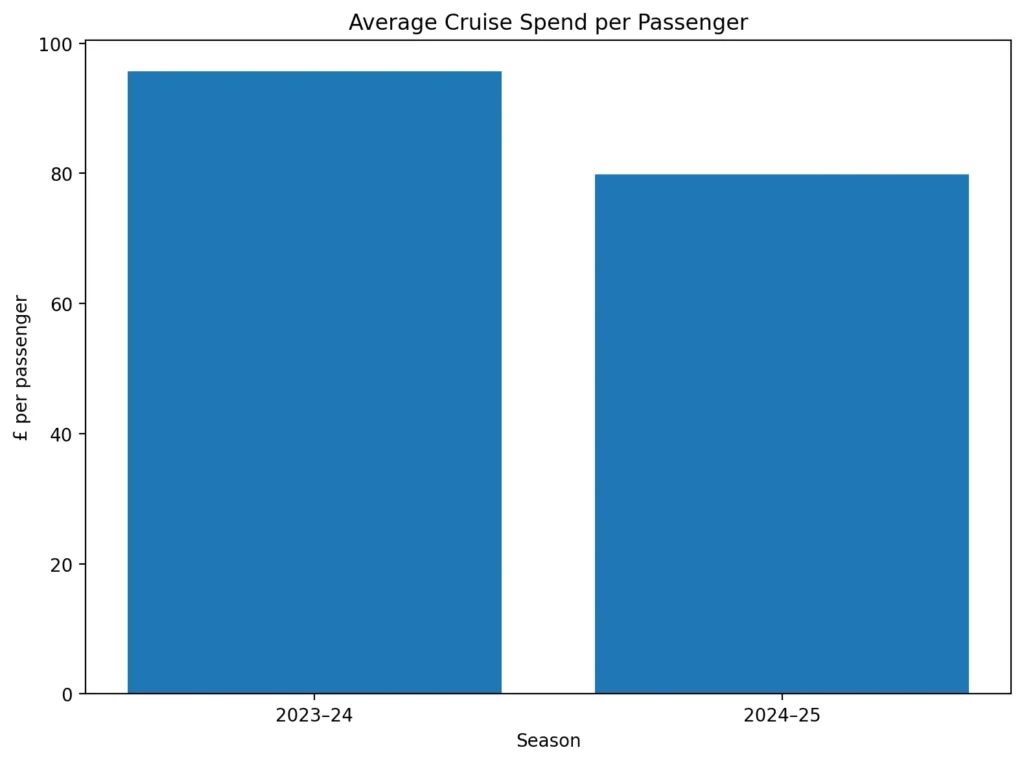

Cruise passengers spent an average of 4.5 hours ashore in Stanley, up from 3.8 hours the previous season. Average spend per passenger fell from about £96 to £79.80, and total cruise passenger expenditure dropped from £7.3 million to £5.5 million. Shopping made up 53% of cruise spend, while tours made up 35%.

That is one of the most interesting shifts in the whole dataset. Passenger numbers only dipped a little. Spend fell much harder. The report explicitly links that to a sharp drop in spend on tours, partly offset by more shopping in Stanley. So the latest cruise story is not “demand collapsed.” It is “visitor behavior changed.”

The expedition side of cruise is also worth watching. In the same 2024 report, the Falkland Islands Tourist Board says 16,148 cruise arrivals, or 22.7%, came on expedition ships in 2024–25. Of the 136 ship arrivals, 103, or 76%, visited at least one destination outside Stanley.

For camp destinations, West Point accounted for 37% of calls, Saunders 24%, and New Island 20%. Those numbers matter because they show how much of the cruise market is not just Stanley footfall. It is also feeding outer-island visitation.

Where Falkland Islands visitors come from

Land-based leisure markets

The UK remains the core land-based market.

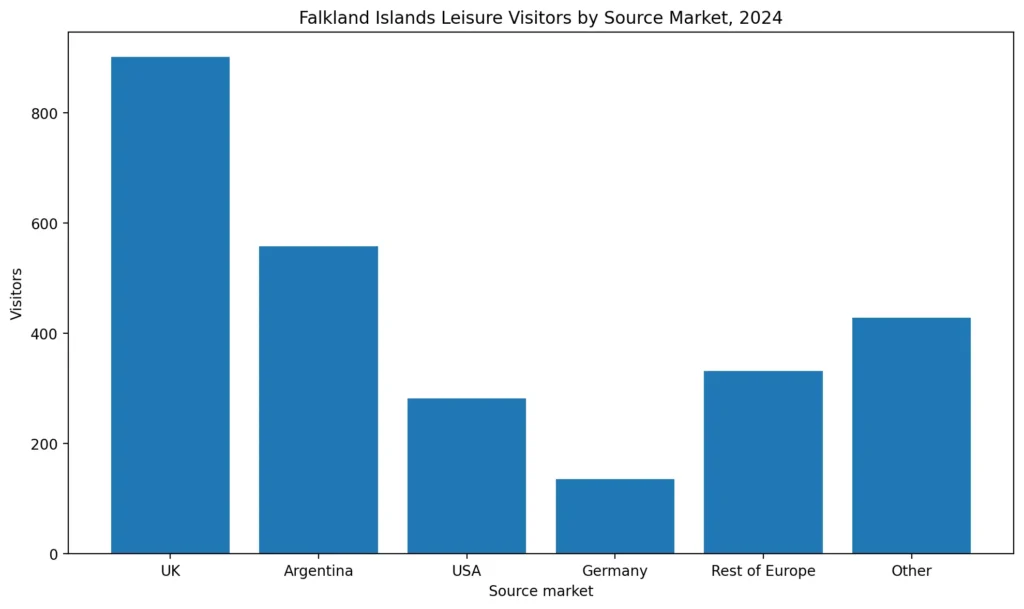

The official 2024 report says the top leisure market was the UK with 902 arrivals, equal to 33.5% of all leisure visitors. Argentina followed with 558 arrivals, or 20.7%, then the USA with 282, or 10.5%. Germany more than doubled year over year to 136 arrivals, and the report also notes Chile rising into the top five markets at 5% share.

That mix matters for content strategy and tourism targeting. It means the site is not only speaking to one English-speaking long-haul audience. The latest numbers support useful country-specific travel content around the UK, Argentina, USA, Chile, and Germany, especially where trip planning or access patterns differ.

Cruise passenger markets

Cruise demand is much more concentrated.

In the 2024–25 season, the official report says the USA was by far the largest cruise source market with 30,477 passenger arrivals, equal to 43% of the total. The UK was second with 6,372, and Canada was close behind with 6,154. Germany, Australia, Argentina, China, Mexico, Brazil, and Switzerland rounded out the top ten.

That is a strong clue for any publisher or operator working in cruise content. If the goal is cruise-oriented reach, the English-language North American segment is the main volume play.

How visitors arrive and what that says about trip planning

Transport mode data adds another useful layer.

The 2024 report says LATAM via Chile carried 1,507 leisure tourists in 2024, or 55.9% of all leisure arrivals, while the RAF Air Bridge brought 668, or 24.8%. The report also notes a big spike in “Other Air” because of a special next-of-kin visit from Argentina in December 2024.

For travel planning, this tells you two things. First, LATAM remains the main commercial route for leisure traffic. Second, UK-oriented travel is still strongly linked to the airbridge. That split supports building route-specific content around both. It also confirms that air-access content is not just a broad topic. It is one of the core structural topics in Falklands travel demand.

Length of stay, spending, and economic weight

The strongest economic signal in the 2024 report is not the biggest raw number. It is the spending relationship between different visitor types.

The official 2024 report says leisure visitors spent £6.9 million in 2024, while cruise passengers spent £5.5 million in the 2024–25 season. That means 2,695 land-based leisure visitors generated more total spend than 71,278 cruise passengers. Even without running new calculations, that tells you air-leisure travel has much heavier economic weight per visitor.

The same report says the average leisure stay was 14.5 nights. It also says Chilean visitors stayed the longest at 23 nights, while Argentine visitors stayed the shortest at around 5.7 nights. UK visitors stayed about 16 nights. Those differences matter because market mix changes can affect local revenue even if arrival counts do not move in the same way.

There is one caveat here that is worth stating clearly. The 2024 report contains two different figures for average leisure spend per night. The brief summary on page 4 says £159, while the key facts table on page 5 gives £204.18. Both figures appear in the same official publication. The safest move is to quote the total leisure spend, which is consistently reported as £6.9 million, and treat the per-night value with caution until the Tourist Board clarifies the discrepancy.

Domestic tourism and accommodation performance

Domestic tourism is smaller from an external travel-marketing perspective, but it still matters for the overall tourism economy.

The 2024 report estimates 10,896 domestic tourism trips in 2024, down sharply from 16,919 in 2023. Those travelers spent 23,300 nights away from home, with an average trip length of 2.1 nights, and total domestic tourism expenditure held around £1.4 million. Average spend per trip rose to £131, up from £80 in 2023.

Accommodation data also moved up. The official 2024 report shows serviced accommodation room occupancy at 35.5% and self-catering unit occupancy at 39.4%. Those are annual occupancy figures, so they should not be read as peak-season availability. But they do show a healthier accommodation picture than the post-pandemic recovery phase.

What the latest data suggests for the next few years

A few patterns stand out from the latest official numbers.

First, the Falklands now look like a recovered but capacity-sensitive destination. Land-based tourism is back strongly, but it still depends on a relatively small number of routes, properties, and planning windows. The statistics do not just show demand. They also hint at how easily that demand can concentrate.

Second, cruise remains the volume engine, but it is not automatically the strongest spending engine. If cruise behavior shifts toward less touring and more casual shopping, total arrivals may stay strong while local yield softens. That is already visible in the 2024–25 data.

Third, the source-market mix is broadening in useful ways. Germany, Chile, and the USA all showed strong growth in the latest land-based data. That gives content publishers a real reason to build more market-specific planning pages, not just one generic Falklands guide.

Data caveats and how these numbers were collected

One reason the Falklands tourism data is useful is that the methodology is clearly published.

The official 2024 report says the dataset draws on:

- customs and immigration data for overnight visits and length of stay

- an air visitor survey at Mount Pleasant Airport with an annual sample of about 400

- a cruise visitor survey at the Jetty Centre with an annual sample of about 600

- a domestic tourism survey with an annual sample of about 200

- an accommodation occupancy survey

- monthly FIGAS leisure-flight data

That is a solid base for a small destination, but it also means some parts of the dataset are sampled rather than full census counts. So the best way to use this page is as a high-quality directional and comparative source, especially when you stay close to the official wording and published tables.

Final takeaway

The latest official numbers show a Falklands tourism market with two very different strengths. Cruise still brings the biggest visitor volume. Land-based travel brings the deeper stay and stronger value per visitor.

In 2024, the islands recorded 2,695 land-based leisure visitors, one of the strongest years on record, while the 2024–25 cruise season brought 71,278 passengers. Combined direct expenditure still topped £16.1 million, even with softer cruise spend.